EMI Calculator: The best EMI Calculator for home loan, personal loan and car loan in India to calculate EMI, interest rate and total payment. It also generates loan amortization schedule and charts.

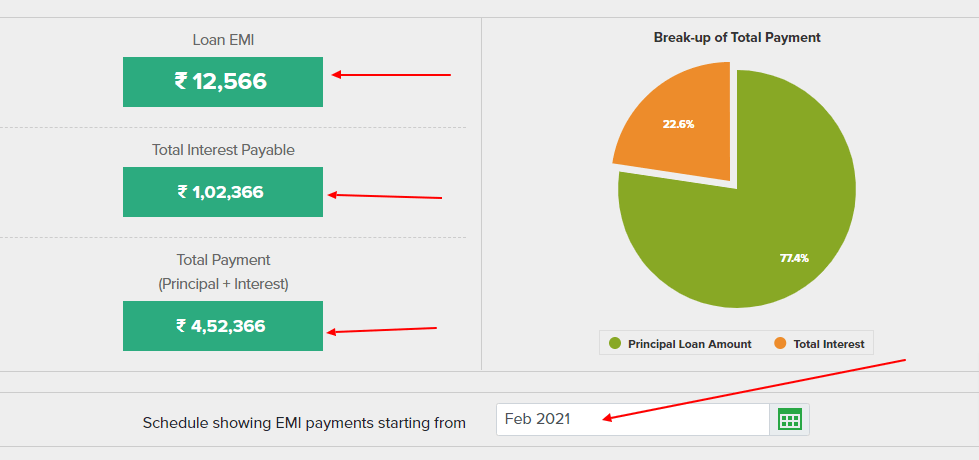

Loan EMI

₹24,959

Total Interest Payable

₹34,90,279

Total Payment

(Principal + Interest)

₹59,90,279

How to use EMI Calculator for Home, Personal and Car Loans?

Use our EMI calculator for home loan, personal loan and car loan to know your Equated Monthly Installments along with amortization and interacted charts. Simply enter principal loan amount, loan term and interest rate to get EMI calculation and amortization schedule. Following are easy steps to calculate EMI, interest rate and total payment:

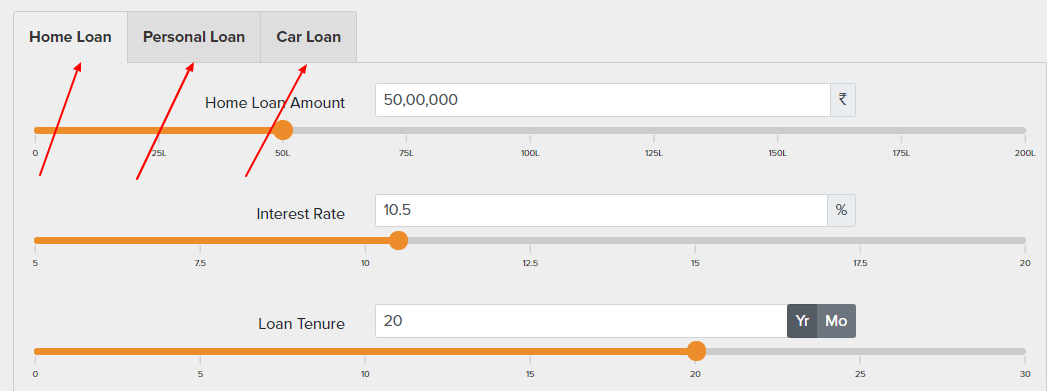

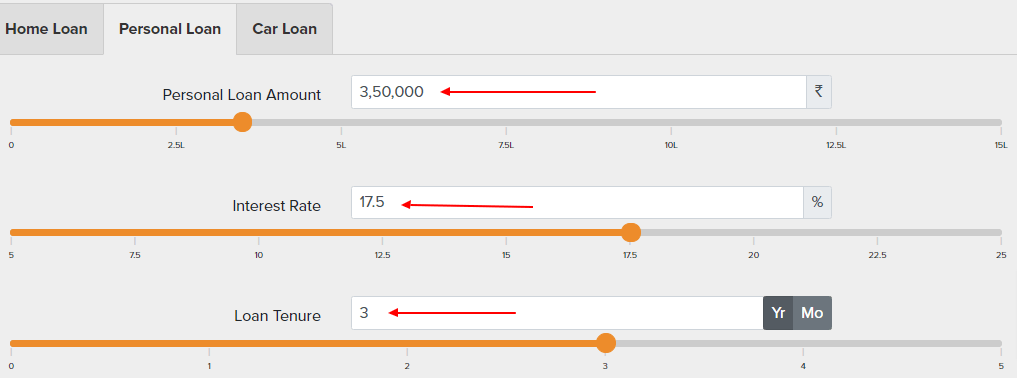

Step 1: Select loan type from home, personal and car loan tabs.

Simply select a loan from tabs (home loan is default) to calculate EMI and interest rate.

Step 2: Enter principal amount, loan tenure and interest rate.

Use slider or manually enter values for principle amount, loan tenure in years/months and interest rate.

Step 3: Get loan EMI, total interest payable and total payment.

Once all done, you will get loan EMI, total interest rate and total payment such as principal + interest.

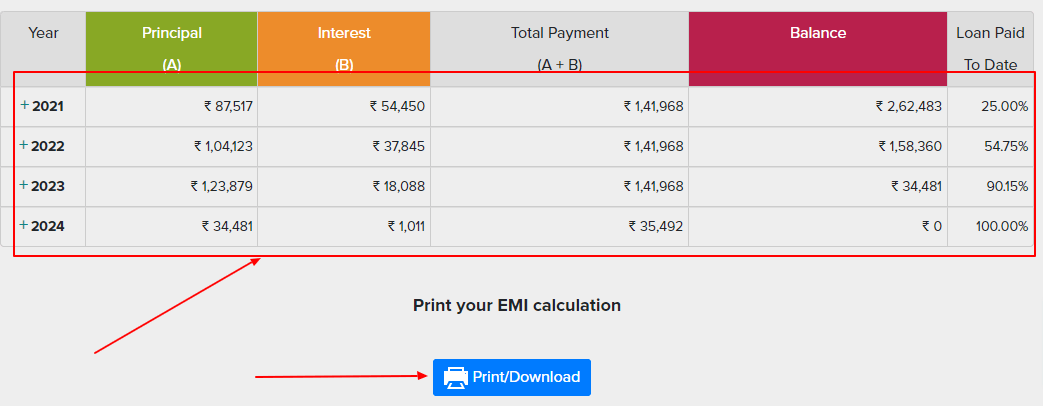

Step 4: Check and download EMI calculation, charts and amortization schedule.

Click on the print/download button to Download or print your EMI calculation with complete loan amortization schedule.

Financial Tools

What is EMI Calculator?

EMI is an acronym used for Equated Monthly Installment which is an amount paid every month by the borrower to the lender. EMI consist of two parts one is the principal amount and the other is the interest which is calculated and paid every month.

EMI that is paid remains fixed however, the amount paid toward principal and interest changes as months goes by. In the EMI paid the interest is higher than the principal amount and as months goes by and loan progresses the principal amount gets decreased as a result of the interest also decreases. This process continues till the entire amount is paid off.

The duration of EMI generally differs from case to case. It can be as short as three months to two/seven years. Sometimes it can also go for more than 10 years.

The EMI calculator is a device which helps one to calculate the EMI that need to be paid out every month. In order to calculate the EMI, there is some information that we need to have such as:

(i) Total cost of the product

(ii) Interest rate charged for EMI and lastly

(iii) The tenure within which one has to finish making the full payment of the product purchased.

This information helps one to understand the monthly amount that had to be paid to the lender and also how much from the total EMI goes to principal amount and interest. There is another point that needs to be looked at is generally the interest rates charged by lender come with two options; one is floating interest rate and the second one is fixed interest rate. Sometimes the lender gives the option for the borrower to choose what rate at which interest need to be calculated. Floating rate is beneficial if the rates fluctuate and if there is a decreasing trend as lesser interest only need to be paid. However, it is equally risky if the interest rates go high leading to paying a high interest. Hence it is safer to opt for the fixed interest rate which remains same irrespective of the market condition.

How to use EMI Calculator?

The EMI calculator is simple and easy to operate. There are three things that are required to calculate the EMI, they are the (i) P= principal or the loan amount, (ii) I- Interest rate per month and finally (iii) N= the number of installments. With the help of this information, one can calculate by feeding the details in the EMI calculator. Generally, the EMI comes has a lesser amount if the duration of the loan taken is more but if the duration is smaller than the amount will be more.

One can decide the duration to be taken based on his or her ability to repay the money. The EMI is calculated based on the formula:

EMI = P × I × (1 + I)n/((1 + I)n – 1)

However while using the calculator one need not use this formula rather just enter the right figures in the given section and one a click of the button the EMI amounts are generated for the complete loan period.

The EMI calculator displays the following information when calculating they are;

- All years for which the loan is taken

- Principal amount

- Interest

- Total payment (principal + interest)

- Balance the loan amount after each EMI and lastly

- Percentage of the loan paid out of the total loan.

This chart without a doubt given every borrower an understanding on how the EMI is calculated and how much of interest they pay out every month for the loan money they have taken. This will surely make the borrower create an awareness has to how to manage his or her monthly income and plan out the EMI payments. Sometimes the EMI calculator also shows a graphical depiction of the same information both in pie charts and in bars for easy reference. Every other bank comes with EMI calculator which anyone of us can use it on our own as it is that simple to fill in the figures and calculate the amount.

Floating Rate EMI Calculation

When taking Equated Monthly Installment there is always an interest associated with based on which it is calculated. This interest comes with two options, i.e. (i) Fixed rate and (ii) Floating rate. The borrower is generally giver the option to choose between the type of rate based on which the EMI has to be calculated.

Floating rate is otherwise known as adjustable or flexible or variable rate. The interest rate under this category fluctuates based on the market- lending rate. Market lending rate or otherwise known as Marginal Cost of Lending Rate (MCLR) is based on multiple factors including the repayment ability. The benchmark of MCLR is generally revised regularly by the banks according to the market conditions.

In this case, the borrower has both risk and benefit in it. If the market lending rates go down then the rate of interest calculated will be lower, as a result, the borrower pays lesser interest but it can also happen the reverse. If the rate of interest goes really high then the borrower is at the disadvantage of paying higher interest and if this is the scenario then the EMI will also increase as a result it becomes very expensive.

Fixed rate is much simpler were a standard rate is fixed at the time borrowing of the money and that remains the same throughout the loan period irrespective of the MCLR. Unlike floating rate, there is no uncertainty in fixed rates.

As mentioned the floating rate has it is own advantages and disadvantages. Generally, this floating and fixed interest rate option come when a person is availing for the home loan. One generally needs to analyse the future situation before taking a decision to go for a floating rate otherwise, it is always wise to go for fixed ass there is no uncertainties involved and can avoid risk.

EMI Calculator FAQ

What are the features of EMI calculator?

This EMI calculator is all in one loan EMI calculator for home loan, personal loan and car loans in India. It has many features, where users can get amortization schedule , charts, EMI calculation, interest rate and total payment calculation in matter of seconds.

How can i calculate EMI calculation for personal loan?

Simply select personal loan tab, then enter loan amount, tenure in months or years and interest rate to calculate EMI calculation for personal loan. You can also select custom date for showing EMI payments schedule.

How to Download loan EMI Amortization schedule?

Once your EMI calculation done, simply click on the download/print button to download loan amortization schedule in pdf format.

What is the EMI Calculation formula?

EMI calculation formula is EMI= [P x I x (1+I)^N]/[(1+I)^N-1]. Where P is Principal Loan Amount, I is interest rate and N is loan tenure.

How to use it as Home loan EMI calculator?

Select Home loan (default tab), then enter home loan amount, interest rate and loan tenure in years or months by entering values. Once all done, check home loan EMI calculation, total interest and total payment along with interactive charts and amortization schedule.